I Spent Four Years Overengineering Something Simple — And That Was the Point

When I moved to Huntsville at 23, I had negative $800 in my bank account and no real understanding of how money worked.

I remember landing at the airport and my boss asking me to put the rental car on my credit card. I didn't have one. He looked at me like I had just said I didn't know how to drive.

I hadn't really lived on my own for long before that. I didn't understand credit, debt ratios, interest, or long-term planning. What I did have was a job surrounded by engineers twice my age, people who had already made their financial mistakes.

I've always been a sponge. So I started asking them a simple question:

“If you were my age again, what would you do differently?”

Over time, I built a mental list. Build credit early. Pay things off. Don't ignore interest. Start saving before you feel ready. When I got to their age, I wanted to be in a better place than I was then.

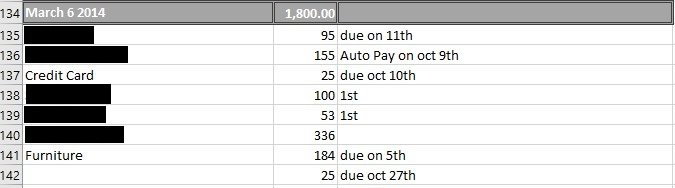

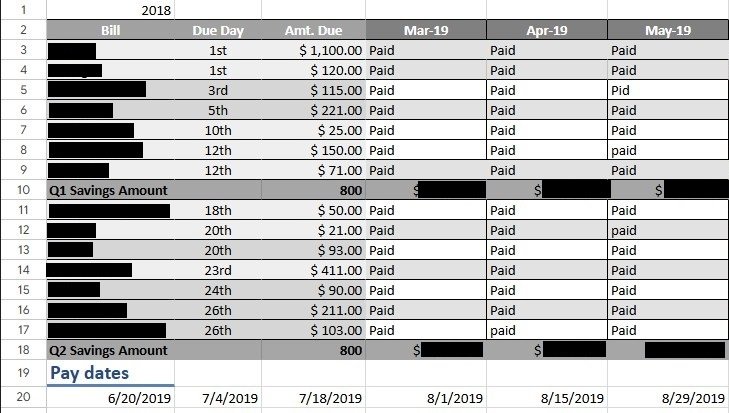

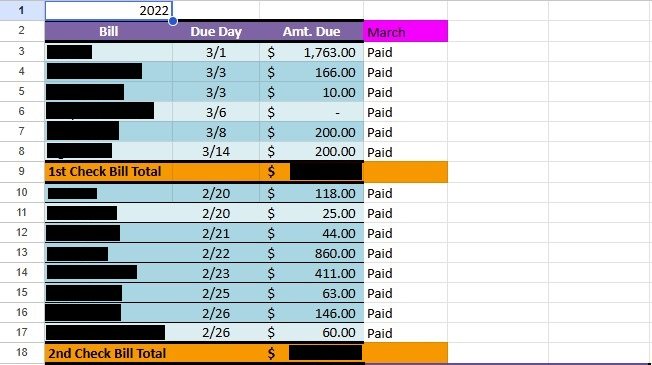

That list eventually turned into a spreadsheet.

The Spreadsheet Era

At first, it was basic. Student loans. A car payment. A few recurring bills. Then my girlfriend (now my wife) moved down, and money got more real.

We bought furniture with terrible interest rates. We had dentist bills. We were trying to plan for bigger things. I started splitting the spreadsheet by paycheck (first check, second check), marking bills as paid, tracking balances, subtracting totals. Eventually I added a savings tab. Then a debt-to-income tracker. Every new thing I learned, I added to the sheet.

When my wife would ask, “How much do we have?” it wasn't a casual question.

It carried weight.

I was trying to save for an engagement ring. We were trying to move forward without slipping backward. Sometimes I had to say no. And I hated how that felt.

The spreadsheet became proof. Not proof that we couldn't do things — proof that there was a plan. That if we stuck to it, we could do more later.

But spreadsheets are clunky. Hard to access on a phone. Easy to ignore.

At some point, I realized I wanted something simpler.

A Moment of Clarity

Around that time, I was approached by a small company that needed help fixing their mobile app.

It was the first time someone had reached out to me about building something outside of my day job. I took it seriously. I stayed up late researching. I learned new tools I had never touched before. I put together a proposal and sent it over.

And then I waited. They never responded.

At first, I thought it was just another missed opportunity. But the more I thought about it, the clearer it became: I didn't actually want to wait around for someone else to decide I was worth building something for. I had already started learning and experimenting. I had already seen that I could turn my spreadsheet into something interactive. If I was going to put nights and weekends into something, it needed to be mine.

That's when this stopped being about helping someone else fix their app and started becoming about building something of my own.

Simplifying and Shipping

Then life sped up.

Around the time we found out we were having our son, time started shrinking. Before that, I could sit in my office late into the night rewriting things. After that, life got real in a different way. It became easier to procrastinate. Easier to say, “I'll work on it when I feel like it.”

The app turned into a background project. I rewrote it more than once. Every time I learned something new, I felt like I had to refactor. I didn't want to build it the “wrong” way. And every time I fixed one thing, I added three more to the list. That list never got smaller.

People would ask me, “Are you ever going to finish that app?”

I had titles. I had experience. But when it came to this, I had nothing to show. Eventually I had to admit something uncomfortable: if I kept building it this way, I might never finish.

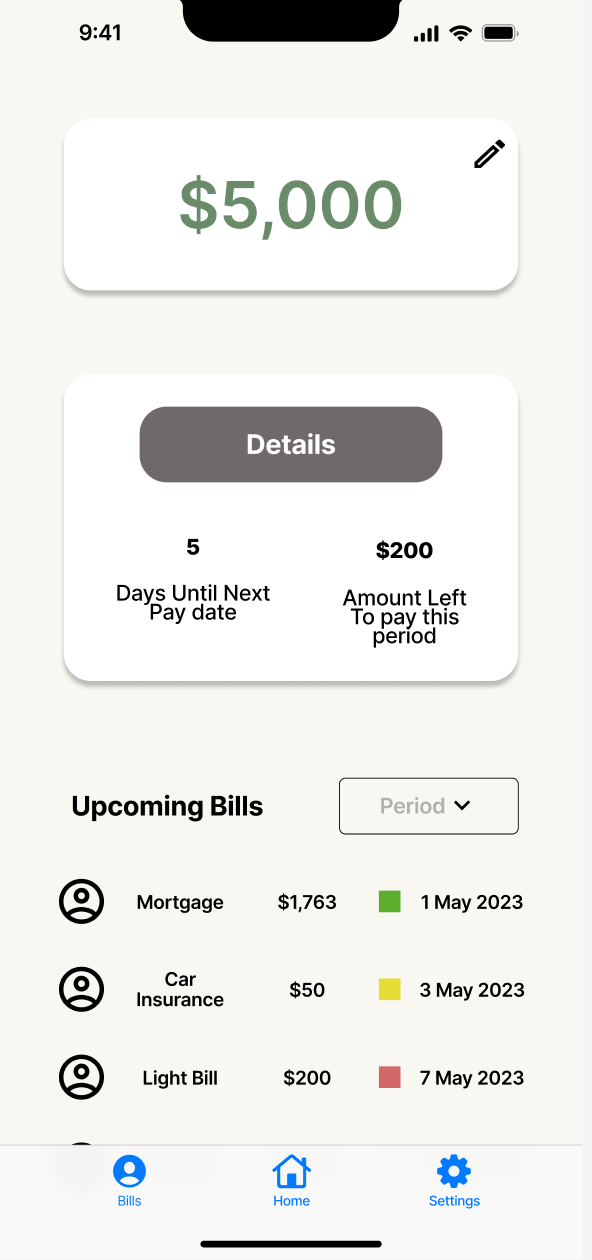

So I cut features. A lot of them. I stepped back and asked a simpler question: what is the point of this app? The answer wasn't complex dashboards or automation or edge cases. It was one thing:

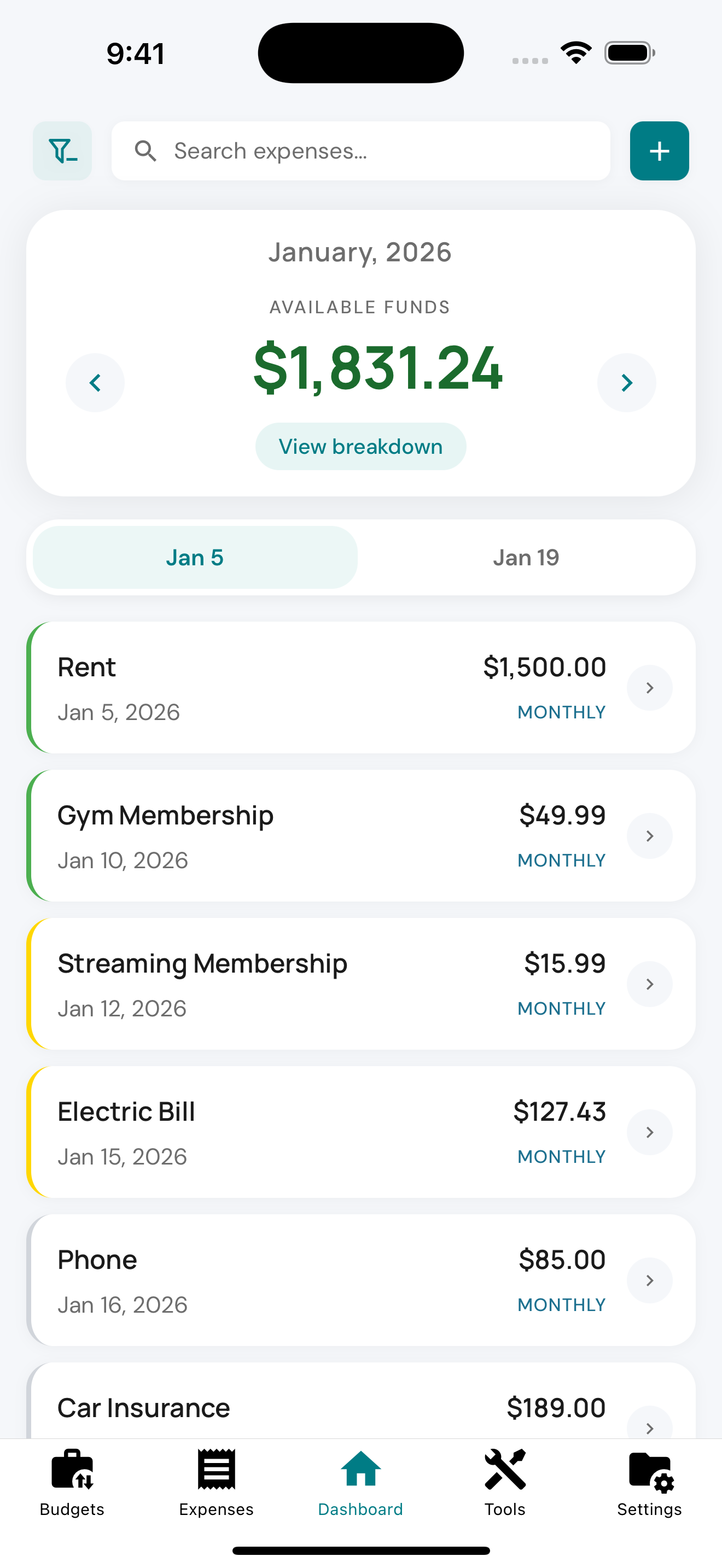

Knowing how much money you actually have until you get paid again.

Not the number in your bank account. The real number, after accounting for the bills that come before the next paycheck.

When I focused on that, everything changed. The list got smaller. Progress became visible. I could check off five things in a night and see the difference the next morning.

I also had to accept that it wouldn't be perfect. But it would ship, and that mattered more.

What It Means Today

When it finally went live, it didn't feel dramatic. There wasn't some huge celebration. It just felt steady, like something I had been carrying around for years was finally sitting on its own. And at the end of all of it, what I built was simpler than I ever expected.

It answers the same question my wife used to ask me when we were sitting at the kitchen table looking at that spreadsheet:

“How much do we actually have?”

Not the number in the bank account. The real number. The number after the bills, after the plan, the number that lets you decide whether you can say yes or need to say not yet.

That's it. It's not connected to a bank. It's not trying to be everything. It doesn't pretend to replace financial discipline. It just shows you the number I used to calculate in my head.

This year, I don't need it to be huge. If 10 to 50 people use it and it helps them avoid that same tension, that's enough.

Finishing it mattered more than perfecting it. And maybe that's the real lesson for me. Sometimes the thing that takes four years isn't complicated. It's just waiting for you to decide it's good enough to exist.

If you've been carrying something unfinished for a while, maybe this is your reminder: cut it down and let it exist.

And if you've ever asked, “How much do we have until payday?” then you'll understand exactly why I built this.

If you want to explore BudgetThrow for yourself, it's available on the App Store — no ads, no bank connections, just clarity when you need it.